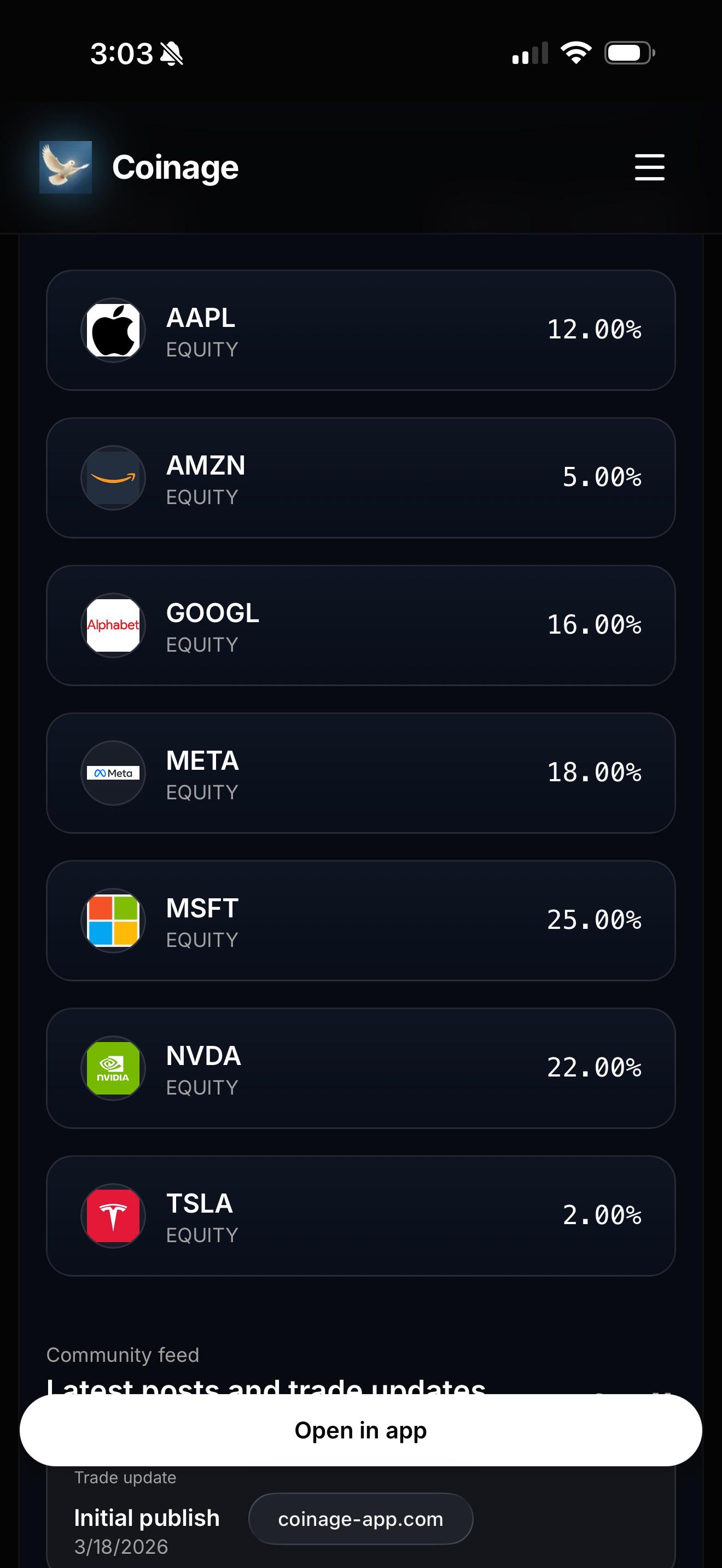

rebel-capitalist

2026-03-18 22:15

Put the fries in the bag

what_could_gowrong

2026-03-18 22:17

6.9420% for tesla because tesla

Training_Marzipan379

2026-03-18 22:17

hahaha

suugami

2026-03-18 22:17

Have you ever heard of a ETF

Metaischeap

2026-03-18 22:22

Alphabet peg ratio is not .76 my boy idk where you got your info google peg is closer to a 1.5-1.8 meta is the cheapest in mag 7 by far

Training_Marzipan379

2026-03-18 22:22

Yeah, but why not create my own?

johnmiddle

2026-03-18 22:23

ETF mags

thegr8lexander

2026-03-18 22:26

Googl should be higher. Extremely undervalued compared to peers

AnalytickAi

2026-03-18 22:26

Interesting weights. Some people will cut AAPL down to 8, it's the most mature of the 7 with the least AI upside near term. Take that and add it to NVDA. TSLA at 2 feels right, more of a sentiment stock than a fundamentals play at this point.

696E6E6F

2026-03-18 22:32

Googl 88% rest 12% Tsla 0%

Alarming_Pension_213

2026-03-18 22:33

Google - 30%

Amazon - 25%

Nvidia - 15%

Microsoft - 15%

Apple - 10%

Tesla - 5%

Meta - 0%

Icy-Sheepherder-7595

2026-03-18 22:41

Maybe a year ago. CAPEX is high FCF lower. Not at all like how it was before where they were the only Mag7 not burning cash but now they're spending to catch up.

Training_Marzipan379

2026-03-18 22:41

yeah that's trailing PEG from last year's 37% earnings growth, not forward. forward is definitely higher. meta probably is cheaper on a growth adjusted basis you're right. would you flip the two?

Stealthless

2026-03-18 22:41

Microsoft shit af

Icy-Sheepherder-7595

2026-03-18 22:44

Because with an ETF you don't have to worry about rebalancing

Icy-Sheepherder-7595

2026-03-18 22:44

Tesla over Meta? Really?

Blade3colorado

2026-03-18 22:51

Actually, this is quite interesting to me, particularly since it caused me to look at my 3 Fidelity accounts, where I have a total of $2.2 million, albeit, approximately $500k is managed by a Fidelity Team\* (they call it "Fidelity U.S. Large Cap Strategy"). Specifically, I was wondering about the %s in this managed account. It should also be noted that I own 2500 shares of NVDA in my regular Fidelity account, along with a 1000 AMZN shares, and 1100 shares of AVGO (which just joined the "trillion" dollar club a month or so ago).

Anyway, I highlighted the "% Of Account" column and of the approximately 150 stocks/ETF this Fidelity Team has me in, VOO is the highest at 9.96%; NVDA 7.83%; AMZN 4.56%; MSFT 4.13%; GOOGL 3.32%; META 2.73%; AAPL 2.40%; and, TSLA .30% (note: AVGO 2.58% and XOM 2.56% were ahead of AAPL and TSLA).

\*Minimum investment of $100k required for an account with this Fidelity Team.

AuthorizedShitPoster

2026-03-18 22:56

100% TSLA (short), 0% rest

Training_Marzipan379

2026-03-18 23:12

that's interesting, nvda on top and tsla basically nothing lines up with what i landed on too. how do you feel about them having amzn above msft? that's the opposite of what i went with. also 2500 shares of nvda is wild lol

TimelyBodybuilder121

2026-03-18 23:16

GOOG>AMZN>AAPL>NVDA>MSFT.

META is being stupid with money. TSLA is kinda falling behind in the EV market.

MSFT is being stupid with decissions but their OS releases are always 1 version sh-t 1 version actually good. 10 was good, so 11 had to be sh-t, 12 will be good.

Since everything is relatively expensive I'll just base it on the ammount of least stupid decissions and user or customer retention.

LFG530

2026-03-18 23:25

Why Apple over Nvidia?

TimelyBodybuilder121

2026-03-18 23:35

Not as exposed in case AI is a bubble. Still involved on the AI side on the neuromorphic R&D side. Way more efficient than the current architecture if someone makes it work properly.

Iphones are still solid. MacOS is a boring, but stable corporate alternative if MSFT keeps making their OS worse.

I-Own-A-Lambo

2026-03-18 23:35

Tesla is not mag7 idgaf what talking head included it, netflix or broadcom take thatcspot

TellFit7415

2026-03-18 23:38

But you have to worry about shit companies like Carvana getting added to the Spy

Excellent_Jeweler_43

2026-03-18 23:46

Can we stop lumping in Tesla with legitimate growth companies?

Prudent-Corgi3793

2026-03-18 23:47

Based on current prices:

- NVDA: 25%

- GOOG: 25%

- MSFT: 25%

- AMZN: 15%

- META: 15%

- AAPL: 5%

- TSLA: -10%

Thin_Cat8817

2026-03-18 23:48

GOOG 25

MSFT 20

AMZN 18

NVDA 15

AAPL 12

META 10

TSLA 0

PERSONA916

2026-03-19 00:18

25% Google

20% Meta

20% Amazon

15% Microsoft

15% Nvidia

5% Apple

0% Tesla

Top 3 I think have the best case for AI improving their primary business. Apple is a fully mature company priced as a growth stock but is still a legit cash cow. Tesla is a meme coin.

HayBailerExtra

2026-03-19 00:19

Google 50% MSFT 25% AMZN 25%

IBangTokyoWife

2026-03-19 00:20

30% GOOG

30% NVDA

15% META

10% AMZN

10% MSFT

4% AAPL

1% TSLA

Hairy_Muff305

2026-03-19 00:22

I would argue that AMZN have an amazing moat. Behind all the AWS, AI, telemed and so on, the online retail business seems to me to be an unassailable monopoly. So when tech shits the bed, AMZN will keep going.

spenga

2026-03-19 00:23

Meta 70%

Google 10 %

Amazon 10%

Nvidia 10%

The rest are zeros

14X8000m

2026-03-19 00:37

More Amazon and Goog, less Microsoft / Meta.

Metaischeap

2026-03-19 00:39

i own both and i trimmed some google bc it ran up a bunch, its still a forever stock its an unreal company, but meta is crazy crazy cheap rn its at a forward p/e of 20 and they will be a winner of ai they have arguably the quickest path to net gain with add optimization and they know how to make an app popular but yeah meta is an 800$ stock today google is about where it should be wouldnt be to crazy for it to go to like 350$ but anything past i would trim a large chunk and wait to reenter

totalnoobass

2026-03-19 00:40

Where's AVGO, and why is TSLA on that list?

Blade3colorado

2026-03-19 00:48

I'm probably prejudiced, as I already own 1000 shares of Amazon. Nevertheless, I suspect some folks think the AMZN negative is their high CAPEX spending, which is projected to be $200 billion+ . . . In effect, the 2 negatives are: 1. Zero to very little cash reserves; and, 2. What's their payback going to be on such huge spending? Conversely, MSFT is down currently due to the lukewarm opinion of Co-Pilot. Specifically, although the AI assistant has gained millions of users, its adoption rate remains a small fraction of the total Office 365 user base, leading analysts to worry that the "AI payback period" may take much longer than originally anticipated.

Thankfully, I bought AMZN at $215 cost basis, so I am not too concerned about it.

flat-waffles

2026-03-19 01:40

You aren't actually shorting tesla are you? I thought there was going to be shenanigans with taking spacex pubic and rolling it up with tesla. that shits going to get massive upward pressure

DiscountAcrobatic356

2026-03-19 01:48

You have 2% too much Tesla

mojitosupreme

2026-03-19 01:58

Agreed on this

LEAPStoTheTITS

2026-03-19 02:03

I’d go heavier on AMZN and googl with less Microsoft but WAY less meta and 0 tsla

But tbh this is kinda dumb for lots of reasons.

lindcookie

2026-03-19 02:30

You're allowed to write shit on the internet

deffjams09

2026-03-19 02:31

Ehh both Elon companies will attract the same type of investor. When space x comes public it will compete with Tesla for a lot of the same investment dollars.

HatersTheRapper

2026-03-19 05:04

I would do 0% TSLA, 50% META 50% NVDA, if I was feeling really wild 10% MSFT and 10% GOOG, I would not buy amzn and I would never buy TSLA if my company had it's valuation my small business grossing between 100-200k a year would be valued at like 43 million dollars.

New_Bad_8760

2026-03-19 05:09

1/3 each GOOG AMZN AAPL

AuthorizedShitPoster

2026-03-19 05:17

No, but the post said if I had to.

Training_Marzipan379

2026-03-19 05:20

I'm a little bullish about Apple because their new chips are killing it, the local LLM performance is impressive.

iXProject

2026-03-19 05:46

Tesla is a legitimate scam company

iXProject

2026-03-19 05:47

META still prints cash, same issue as in 2022, Zuck will capitulate

Not_a_CSIS_agent

2026-03-19 06:11

Catching up to who and to what, exactly? Capex ain’t getting cheaper…

JR-FlowCapGroup

2026-03-19 07:02

I would look at weighing at a different angle. Instead of weighing on either performance or the quality of the business, try weighing them according (under)valuation.

Let's assume company A is undervalued and company B is fairly valued. The growth prospect are the same and they are AI players. I'd consider having a higher weigh percentage for company A compared to company B. Theoretically, if the stock market is correct and evenly distributed, you'll make more money with company a, if this makes sense. Make your high conviction bets, high weighing.

Also, I stopped trying to understand why people keep investing in tesla.

Luuigi

2026-03-19 08:15

Essentially Everyone on this planet loves apple products but stock pickers despise them. Its the other way around for msft.

TimelyBodybuilder121

2026-03-19 08:26

Robo autoban says otherwise.

Icy-Sheepherder-7595

2026-03-19 09:57

They weren't spending as much as competitors on improving their AI products. It's an arms race. They want to catch up to and surpass their competition. What is so hard to understand.

Prudent-Corgi3793

2026-03-19 10:57

If you want specifically Mag 7 exposure, there's the MAGS ETF, but it's terrible, even if you decide you want exactly seven stocks in your portfolio and are too lazy to buy those seven stocks yourself.

The expense ratio is "only" 29 bps, but they use ridiculous return swaps which completely kill their return. I can't think of any reason to do this except so they can be technically considered "diversified", even if this does absolutely nothing to really diversify their portfolio. In the meantime, it means they've trailed just buying the seven stocks by almost 4% per year (and about 20% cumulatively since inception): https://testfol.io/?s=6JU8nboO9Nc

Assuming a $1M investment for 30 years, with even a relatively conservative 10% expected return, that 4% real drag will cost you $11.7M over the life of the investment--more than 2/3 of the amount you would have had otherwise. (If you want to assume the Mag 7 will continue delivering 40% per year--which would never happen--then that will cost you $14 billion over the life of the investment.)

Icy-Sheepherder-7595

2026-03-19 11:16

I was more so referring to just buying VOO, VT, QQQ, etc...

Prudent-Corgi3793

2026-03-20 01:46

Great company. I personally spend a ton of money each year on AAPL products, and I was waiting to upgrade an M5 Ultra with 512 GB for exactly this reason (who knows if it will even get released at this point).

The reason I only kept AAPL at market weight within the Mag 7 is two-fold:

- They have the highest valuation of any Mag 7 (besides TSLA).

- They have the lowest growth rate of any Mag 7 (besides TSLA).

From Fiscal.ai, but other sources tell a similar story:

| Stock | TTM P/E | NTM P/E | Rev CAGR (3 yr) | Dil EPS CAGR (3 yr) |

|:--|:--|:--|:--|:--|

| NVDA | 36.4 | 24.2 | 68.8% | 86.2% |

| AAPL | 31.5 | 28.4 | 4.0% | 10.3% |

| GOOGL | 28.3 | 25.5 | 12.5% | 33.4% |

| MSFT | 24.3 | 21.4 | 14.4% | 21.1% |

| AMZN | 29.1 | 26.3 | 11.7% | 198.3% |

| META | 25.8 | 19.5 | 19.9% | 39.8% |

| TSLA | 352.1 | 181.1 | 5.2% | (-33.2%) |